What Is a Money Calendar? And Why It Works When Budgets Don’t

Writer

Mel Mandara

Editor

Erin Elizabeth Reed

If budgeting has never worked for you, you're not broken.

I want to hold your hand when I tell you this:

Your brain isn't the problem. The tools are.

And I know what you’re thinking…

”that’s the most cliche sh*t I’ve ever heard”

But give me 60 seconds and if you can relate to anything I’m about to say, then maybe… maybe I’m right, just saying.

Okay start the clock…

So, I’ve been searching for the perfect budgeting system for years.

I think I’ve tried everything under the sun. Downloaded six different budgeting apps that all promised to "bring clarity to my money".

I’ve also bought a couple of those $7 budgeting spreadsheet from Etsy/ Stan store, you know, the ones with 47 categories in pastel colors that you always forget to update.

I’ve also watched countless YouTube and TikTok videos about envelope systems and stuffing cash in color coded binders.

And somehow the person in the video is also conveniently selling said binder for 67% off in their Tiktok shop (but you have to hurry because the sale ends in 5 minutes).

There are so many different ways to budget.

And I’ve tried them all. Dave Ramsey would love me…

So then why do none of them seem to stick?

And for fuck's sake, why are there always so many categories? I never understood the need to categorize everything.

Like how am I supposed to know how much to budget for toilet paper?

And what happens if I go $3 over on groceries — do I just... not eat?

What if my car needs gas in the middle of the month and I’ve already "spent" my transportation budget?

I try putting my money into cute little boxes for a week or two, but like clockwork, I end up quitting. Again.

And yes a few months later, the cycle starts over. I feel motivated to get my shit together.

I download a new app and I just know "this one is different".

This one doesn’t have pastel, it’s minimalist. It uses ‘AI’. Jarvis is gonna fix me… right?

Does any of this sound familiar? Why does it feel like nothing works?

Well that’s because every budgeting app is trying to do the same thing — make budgeting easier.

The problem isn't that budgeting is hard.

The problem is that budgets were never designed for a brain like yours. mic drop

The Real Problem Isn't You — It's the Tools

So, here's what actually happens when you try to use traditional money tools:

You forget bills exist until they're overdue.

Not because you're irresponsible but because if something isn't directly in front of you, it might as well not exist. This is called object permanence.

And no, not only babies experience this, it's a real thing that affects most of us, especially those with ADHD.

You get hit with "surprise" charges that weren't actually surprises.

Your car insurance renews. Your annual subscription for that domain you forgot about auto charges. But then, your credit card payment is due.

These things happen on a schedule, but if you can't see the schedule, it feels like whiplash every single time.

You avoid looking at your bank account.

Opening that app feels like opening Pandora's box. There's just too much information, all at once, with no context. Just numbers that end up making you feel behind and overwhelmed.

Time doesn't feel linear when it comes to money.

"Two weeks from now" and "next month" occupy the same vague space and your brain ends up labeling it a "future problem."

This is called time blindness, and it makes planning for bills feel impossible.

If you're nodding along to most of these, there's a good chance your brain works differently than traditional money tools expect.

Many of these patterns are common in ADHD brains.

But I’m not here to diagnose you.

Whether or not you have an actual ADHD diagnosis, the point is the same:

budgeting tools weren't built for you.

Every money tool you've tried assumes you'll remember to use it consistently.

But consistency is the thing your brain struggles with most.

Budgeting apps require daily logging.

Spreadsheets require manual updates.

Even "set it and forget it" systems require you to, you know, set them up in the first place without getting overwhelmed and abandoning the whole thing.

So then…

What is a money calendar and how is it any different?

What Is a Money Calendar?

Here's the simplest way to explain it:

A money calendar shows your money in time — not categories.

That's it. That's the whole thing.

Most budgeting tools organize your money into categories: food, rent, utilities, entertainment, savings.

They make you split your life into neat little boxes and then punish you when real life refuses to fit.

A money calendar doesn't care about categories.

It cares about when things happen.

It shows you: this bill is due Thursday. That subscription renews next Tuesday. Your paycheck hits Friday. Your credit card payment is in 9 days.

Everything lives on a timeline you can actually see.

Both the money coming in and the money going out.

Instead of asking:

"how much should I spend on groceries this month?"

(which requires predicting the future, estimating costs, and pretending inflation doesn't exist),

a money calendar asks:

"what's coming up this week that you need to know about?"

Why This Term Exists

I started using the phrase "money calendar" because I couldn't find another term that captured what I actually needed.

"Budget" implies restriction and categories and math I don't want to do.

"Spending tracker" implies I have to remember to log every transaction like I'm some kind of disciplined finance robot with 9 years of accounting experience.

Like who actually cares about a $5 latte?

Then on the other hand, "envelope system" sounded exhausting and requires cash I don't carry.

But a money calendar?

That's what it actually is.

It's a calendar that shows your financial life in time.

Bills, paychecks, subscriptions, loan payments and all your different forms of income. All laid out where you can see them before they happen.

It's not about control. It's about visibility.

When I can see what's coming, I don't feel ambushed by my own life.

What a Money Calendar Is (and Isn't)

Let's clear this up right now because I know what you're thinking: "isn't this just budgeting with a different name?"

No. It's not.

A money calendar IS:

Visual. You can see your whole month (or week, or day) at a glance. No digging through spreadsheets or trying to remember if you already paid something.

Time based. Everything is organized by when it happens, not what it is. This matches how ADHD brains actually process information, which is in sequences, not imaginary categories with abstract definitions.

Forgiving. If you forget to check it for three days, nothing breaks. It's still there. The information doesn't disappear because you weren't "consistent" or forgot to log those tacos you had 2 weeks ago.

Forward looking. A money calendar tells you what's coming before it happens. Say goodbye to overdrafts. Hasta la vista baby!

Real time aware. Here's the real game changer: a money calendar doesn't just show you what's due, it shows you if you can actually afford it. It compares upcoming bills against your actual bank balance right now. You can see: do I have enough for today? This week? This month after all the upcoming charges hit? You're not guessing. You're not doing math in your head. You can see what your wallet will look like after everything clears.

Tracks what actually matters. You're not logging every coffee or gum. A money calendar tracks your income and recurring expenses, the predictable stuff that shows up on a schedule. Your rent. Your paychecks. Your subscriptions. The bills that repeat. That's the stuff that actually determines if you're okay or not.

What a money calendar is NOT:

A strict budget. There are no spending limits. No categories to stay within. No guilt when life costs more than you planned.

A spreadsheet. You're not doing math. There are no formulas. You're not updating 47 cells every time you buy a margarita. You're just looking at a timeline.

A discipline test. It doesn't require you to be "good" or "consistent" or "on top of things." It exists to help your brain, not judge you.

A fix all solution. It won't magically make your debt disappear or double your income. But it will help you stop feeling like you're constantly drowning.

Why Money Calendars Work for ADHD Brains

Traditional budgeting tools weren't designed with ADHD in mind. At all.

They were designed for neurotypical brains that can:

Remember things without visual cues

Estimate future spending accurately

Maintain consistent habits

Process abstract categories

Plan weeks or months in advance without losing track of time

If that's not your brain, those tools will always feel like you're forcing a square peg into a round hole.

Now, here's why money calendars actually work:

Time blindness gets an external structure

When you have ADHD, "next week" doesn't feel real until it's happening.

A money calendar externalizes time. It turns the abstract concept of "bills are coming" into "here are the specific days things are due."

You're not trying to hold the timeline in your head anymore.

It's right there in front of you.

Object permanence gets a visual anchor

If you can't see something, it doesn't exist.

That's why your bills fall through the cracks. They become invisible until the day they're due (or overdue).

A money calendar makes everything visible.

Your car insurance isn't hiding anymore. It's on Thursday. You can see it. Pay it.

Overwhelm gets narrowed down

Looking at your entire financial life all at once is paralyzing.

A money calendar lets you zoom in. You can look at just today. Just this week. Just the next three days.

You don't have to hold the whole month in your brain at once.

Avoidance gets reduced

The reason you avoid your bank app isn't laziness.

It's because every time you open it, you're hit with too much information and not enough context.

A money calendar is different.

It's not showing you your failures. It's showing you what's next and that's way less scary.

Emotional regulation gets easier

Surprise bills trigger panic and anxiety. Visible bills don't.

When you can see a $200 payment coming next week, you have time to prepare.

You can shuffle money around, pick up an extra shift, or just mentally brace yourself. You're no longer caught off guard.

And when you're not constantly in crisis mode, you can actually think clearly about money.

What This Looks Like in Real Life

Let's compare two versions of the same month.

Without a money calendar:

It's October 18th. You check your bank account and feel your stomach drop. Your balance is way lower than you thought.

Oh. Right. Your car insurance auto renewed yesterday. You forgot that was this month.

And your credit card payment is due... wait, when? You open the app. It was due two days ago. Great. Late fee.

Your rent is coming up soon but you're not sure if you have enough to cover it and groceries and gas. You'll figure it out. Somehow. Like you always do.

You close all the apps and promise yourself you'll "get better at this."

You feel stressed. Behind. Like you're failing at something that’s supposed to be “basic”.

With a money calendar:

It's October 18th. You open your money calendar.

Your car insurance was yesterday. You saw it coming last week, so it wasn't a surprise. Check.

Your credit card payment is on the 20th which is two days from now. You can see you have enough to cover it.

Rent is due on the 1st. The calendar shows your current balance, the upcoming charges, and what you'll have left after everything leaves your bank account. You can see you'll have $340 remaining for groceries and gas. Not guessing. Knowing.

You're not operating in the dark. You know what's coming and you know if you can handle it.

You can breathe.

This is the difference. It's not about having more money. It's about seeing the money you have in a way that actually makes sense to your brain while also knowing, in real-time, if you're okay.

How a Money Calendar Helps With Debt

If you're in debt, the emotional weight is even heavier.

Every credit card payment feels like throwing money into a void. Every student loan payment feels endless. You can't see progress. You can't see when it will end.

This is where a money calendar becomes even more powerful.

Because debt isn't just about numbers. It's about time.

When you owe $5,000 on a credit card, that's not tangible information. But when you can see "52 more payments" laid out on a timeline? It starts to feel real. It's still hard. But now it's visible.

You can see the end.

And here's what happens when you can see the end: you stop feeling like it's pointless.

Timelines reduce shame

Shame thrives in the vagueness. "I'll be paying this off forever" is a story your brain tells when it can't see the actual timeline.

A money calendar shows you the truth. It might take two years. It might take four. But it's not forever. And seeing that truth is kinder than the story shame was telling you.

Progress becomes visible

When you can see each payment marked off on a calendar, progress stops feeling theoretical.

You paid October's payment. Cool. One more down. You can literally see the number of payments shrinking over time.

That's motivating in a way that a notification stating "you paid $127 today" just isn't.

You can plan around debt without drowning in it

Debt payments are just another thing that happens in time. They're on your calendar, just like rent and utilities and your phone bill.

This doesn't make them go away. But it does make them manageable. You're not carrying the weight of "how am I going to pay everything" in your head all the time. You can see what's coming and when.

Where Subbie Fits Into This

If you've made it this far and you're thinking "okay, this makes sense, but how do I actually do this?" This where Subbie comes in.

Subbie is a money calendar built specifically for people who feel overwhelmed by traditional money tools.

It's not another budgeting app pretending to be different. It's actually different.

Here's what makes Subbie a money calendar:

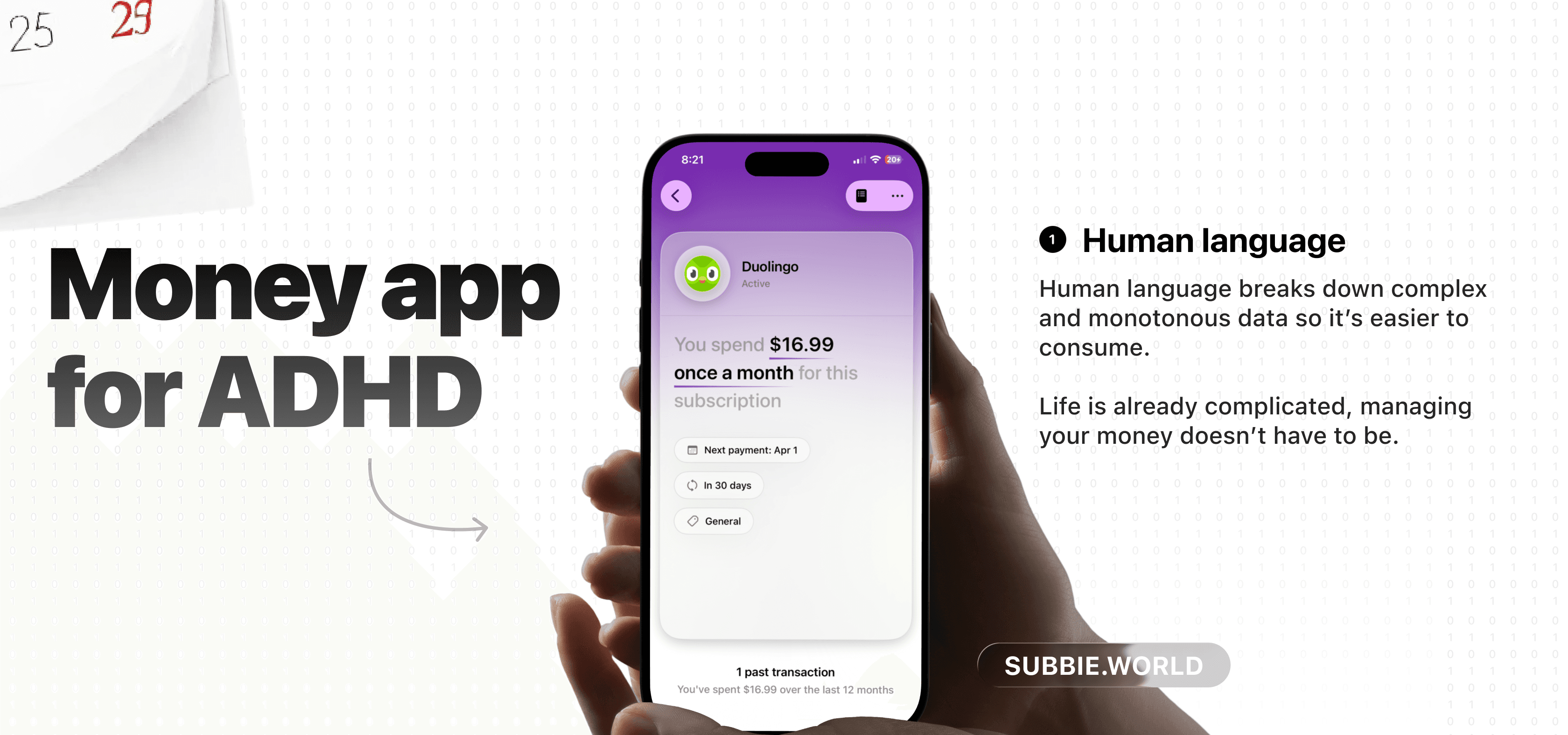

It shows your financial life on a visual timeline.

Bills, paychecks, subscriptions, BNPL plans, debt payments, they are all in one place. You can see what's due Thursday, what renews next week, and when your debt will actually be paid off. With an end date. Not "someday." An actual real date.

It talks to you like a human, not a bank.

No cold fintech language. No "optimize your cash flow" or "maximize liquidity." Just: "You have $230 left after your bills this week." The kind of language that doesn't make you feel stupid.

Widgets with a human touch.

Most money apps show you logos and balances that trigger anxiety every time you glance at your phone. Subbie's widget not only speaks in plain language but allows customizations that matches your vibe. This gamifies your finances which is a huge plus because you deserve to feel good about money, not stressed every time you unlock your phone.

It predicts what's coming based on your patterns.

You're not manually entering the same bills every month. Subbie learns: your rent is the 1st, your phone bill is the 15th, that random subscription you forgot about renews on the 22nd. It tracks the pattern so you don't have to remember.

Subbie tracks multiple income sources.

Freelance gig? Side hustle? Regular paycheck? Sporadic client payments? You can track all of them. And here's the cool part: Subbie's auto match feature learns which payments are income. Once you mark a payment from a specific source as income, it automatically tags future payments from that source. So if you get paid via Venmo, PayPal, or direct deposit from multiple clients, you're not manually logging every single one. It learns the pattern.

It shows you what your wallet looks like after everything clears.

This is the game changer. You can see your actual bank balance right now, compare it to what's coming, and know exactly what you'll have left after all the charges hit. Today. This week. This month. Not guessing. Knowing.

You can see just what you need to see.

Overwhelmed by the whole month? Look at just today. Or this week. Or the next three days. You choose the view that doesn't make your brain shut down.

Extra payments actually change your timeline.

If you throw an extra $100 at your credit card, Subbie recalculates and shows you your new payoff date. Progress isn't theoretical. You can see the finish line moving closer.

Subbie tracks everything in one calendar.

Subscriptions with auto renew dates. BNPL plans with end dates. Debt with actual payoff timelines. Bills that repeat. You're not juggling five different apps or trying to remember what's where. It's all there.

You can forget to check it and nothing breaks.

Most money tools punish inconsistency. Subbie doesn't. If you forget to open it for a week, your information is still there. Your timeline didn't disappear. You're not starting over.

There's a community of people who get it.

You're not alone in this. Other people who forget bills, avoid bank apps, and feel "bad with money" are figuring it out together. No judgment. No finance bros. Just people trying not to feel ambushed by their own lives.

It was built for brains that forget, avoid, and struggle with traditional money systems.

Because those brains aren't broken. They just needed a tool that worked with them, not against them.

It was built for brains that forget, avoid, and struggle with traditional money systems.

Because those brains aren't broken. They just needed a tool that worked with them, not against them.

Common Questions About Money Calendars

"Isn't this just budgeting?"

No. Budgeting is about categories, limits, and restrictions. A money calendar is about visibility and timing. You're not tracking every dollar you spend. You're seeing when money comes in and when it goes out.

"Can this work if I'm in debt?"

Yes. Actually, it can work better if you're in debt because debt repayment is inherently time-based. Seeing your payoff timeline makes the whole thing feel less impossible.

"What if my income changes every month?"

That's fine. A money calendar isn't about predicting exact amounts. It's about seeing the pattern of what's coming. If you get paid irregularly, your monthly calendar doesn’t change.

"What about variable expenses?"

A money calendar doesn't track every variable expense and that's on purpose. You're not logging every coffee, every grocery trip, or every random Amazon purchase. That's exhausting and it's why budgeting apps fail.

Instead, a money calendar focuses on your recurring money.

These are the stuff that happens on a schedule. Your rent. Your bills. Your income sources. Your subscriptions.

The predictable income and expenses that actually determine whether you're okay or not.

The random stuff?

That lives in the gap between what comes in and what goes out.

And when you can see that gap clearly, you know what you have left to work with.

"Do I need to be disciplined to make this work?"

No. That's the whole point.

This system doesn't rely on consistency or discipline.

It relies on visibility. If you forget to check it for a week, nothing breaks.

The information is still there when you come back.

"What if I'm really bad with money?"

You're probably not as bad with money as you think.

You're probably just using tools that don't match your brain.

A money calendar doesn't fix everything.

But it does make it way harder to feel blindsided by your own financial life.

You're Not Broken

So let me wrap this up with a couple affirmations:

Firstly, you don't need to be perfect with money.

You don't need to remember everything.

You don't need to be consistent or disciplined or "better."

You just need a way to see your money that doesn't make you want to hide from it.

Budgets don't work for everyone. Spreadsheets don't work for everyone. Not everything is for you and that’s completely okay.

A money calendar is different because it's built for people who forget.

For people who avoid. For people whose relationship with money has been defined by shame and inconsistency and feeling behind.

If this sounds like what you've been missing, Subbie was built for exactly that.

Not to fix you. But to meet you where you are.